Temporary differences on settlement reports CIT is a common issue that businesses often encounter in the process of filing tax. This difference can cause breakdowns in financial management, increasing costs, and even affect the reputation of the business.

To solve this problem, the processing of temporary differences on settlement report corporate income tax is very necessary. In this article, we will look at the causes that led to temporary differences on settlement report corporate income tax and how to handle them to ensure that taxes are accurate and avoid the legal risks.

1. Manual handling temporary differences on settlement CIT

Temporary differences related to revenue is one of the common problems that businesses often encounter when reporting income tax settlement business. This gap may appear when business recorded revenue on other financial statements with revenue is calculated at the tax settlement. This can make the business faced with the taxes, penalty or tax audit, cause the legal risks and affect the credibility of the business.

To handle temporary differences related to revenue settlement reports CIT, first business need to find out the cause of this difference. Possible causes are due to errors in the process of revenue recognition or due to differences in the time of calculation of revenue between financial reporting and tax settlement.

1.1. Related to revenue

The account temporary differences, and the only goal adjustment on settlement CIT

On settlement and CIT, the account temporary differences and indicators of adjustment is determined based on the difference between tax law and accounting law. There are a number of situations that cause this difference, such as:

The time recorded export sales of differences between tax and accounting

Purchase and sale contracts regulations, the buyer is the right to return the products, goods and services.

Trade discount has not been allocated to year accounting, but was accounted for in the accounts 521 ago when the financial statements, and how to recognize revenue for rental property differences between tax and accounting.

In addition, the sale of goods, providing services incurred obligations in the future and sales volume bonus points are also different rules between tax law and accounting law.

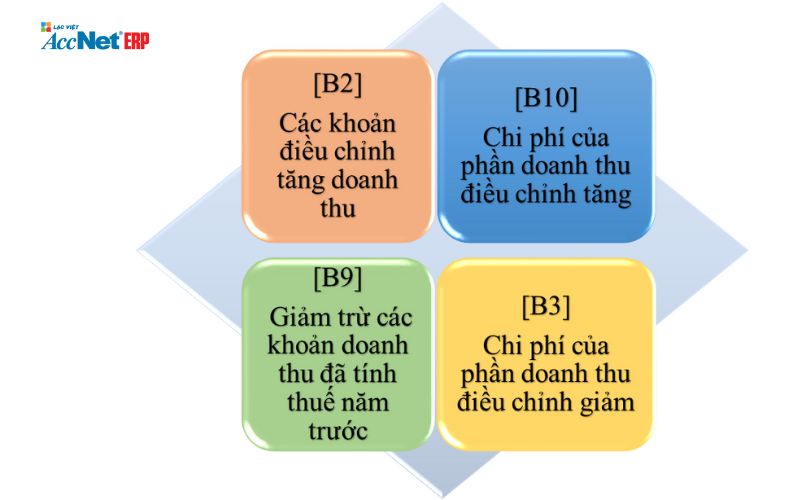

Adjusting of the corporate income tax of the reporting year and the year adjustment

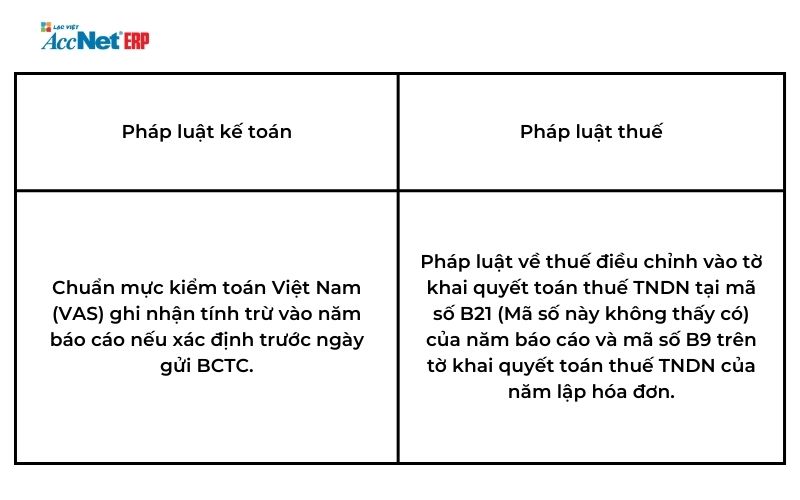

In the process of adjusting income business code of [B2] and [B10] will be adjusted in the reporting year. Meanwhile, the code number [B9] and [B3] will be adjusted in the year of adjustment.

The norms regulating settlement reports CIT

However, accounting revenues and expenses are not adjusted. (The only goal is quoted from model no. 03/CIT, circular no. 80/2021/TT-BTC dated July 29, September 9, 2021 by The minister of Finance) is:

[B2]- The adjustment amount, increase revenue;

[B10]- Cost of revenue adjustments;

[B9]-Reduced the revenue tax year ago;

[B3]-Cost of revenue adjusted up )

Table setting identify temporary differences and the calculation for the deduction is made.

Taxable revenue should be recorded and adjust on the code [B2] the reporting year and the code number [B9] in the adjustment.

Respective expenses also need to be extracted before to adjust to the code [B10] the reporting year and the code number [B3] year adjusted in accordance with point 2.20 paragraph 2 of circular no. 96/2025/TT-BTC.

The end of the contract, or arising turnover, enterprises need to calculate and determine the exact amount of the actual cost to adjust to increase or decrease the cost based on the invoices and receipts from legal practice has arisen.

The account temporary differences are accounting as follows:

In the reporting year, the accounting with the account temporary differences is done by:

Debt TK 8211 - Cost CIT current

Have TK 3334 - CIT to record the number of INCOME tax payable under the tax law.

Then, accounted for by:

Debt TK 243 - Assets deferred INCOME tax

Have TK 8212 - tax Expense deferred INCOME to record the number of CIT difference due by tax law than the law on accounting.

In this adjustment, when revenue and the actual cost incurred, the accounting with the account temporary differences is done by:

Debt TK 8212 - Cost deferred INCOME tax

Have TK 243 - tax Assets deferred INCOME to recorded assets deferred INCOME tax is reversed when the number of CIT difference due under the tax laws smaller than accounting law.

1.2 specific examples to guide how to handle the situation related to revenue.

Handling instructions about the time recorded export sales between tax and accounting

Example 1:

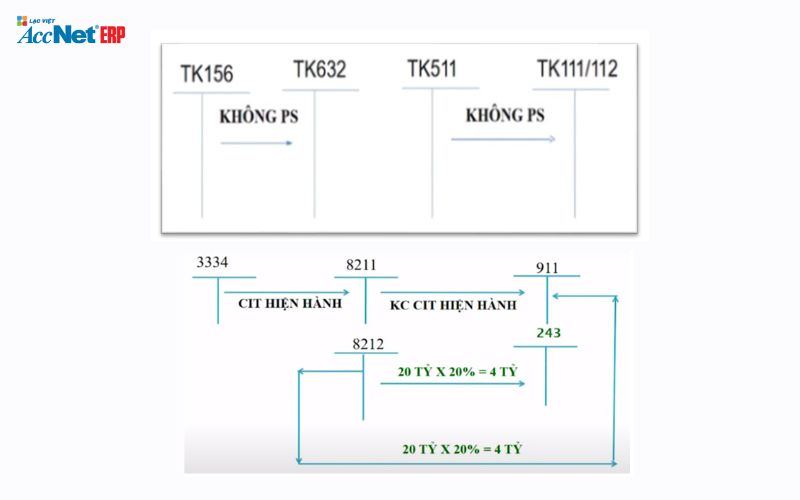

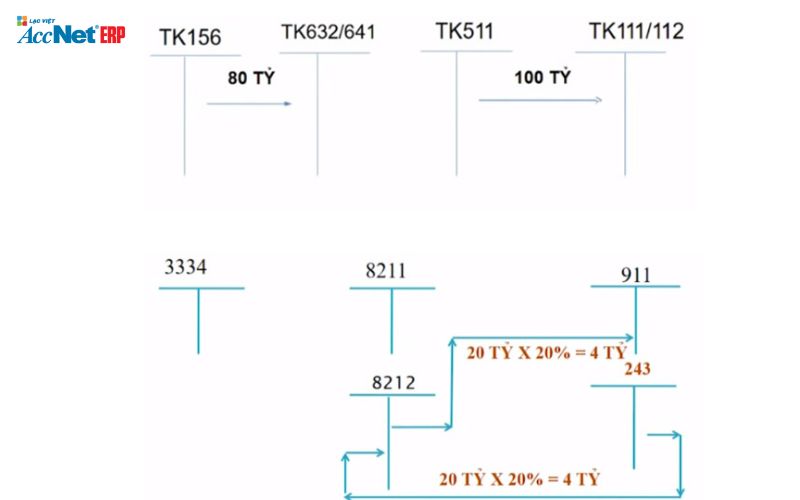

Date 31/12/2021 business has a batch export has not moved through the ship's rail, but the procedure has been completed customs with the sale price is $ 100 billion, the price of capital and the cost of delivery is 80 billion.

To adjust the difference with respect to example 1, we need to perform the following steps:

Step 1: Determine the revenue and expenses related to sales transactions

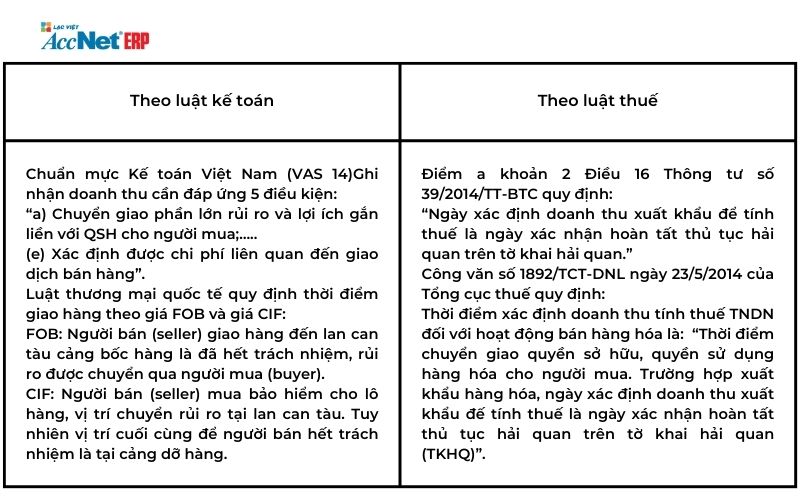

Under circular no. 200/2014/TT-BTC, export revenues is determined at the time of completion of the customs procedure of the customs declaration (TKHQ). In this case, the revenue of the business is $ 100 billion.

Costs related to sales transactions, including the cost of capital and cost of delivery. As for example, the capital cost and the cost of delivery of the business is 80 billion.

Step 2: Calculate the difference

The difference is calculated by the formula: Difference = Sales - Costs related to the sales transaction = $ 100 billion - 80 billion = 20 billion.

Step 3: adjust The difference in business results

The difference 20 billion will be adjusted on the results of business at the profit before tax. If the difference is interest, it will be added to the profit before tax to calculate tax. Conversely, if the difference is hole, it will be deducted from profit before tax to calculate tax.

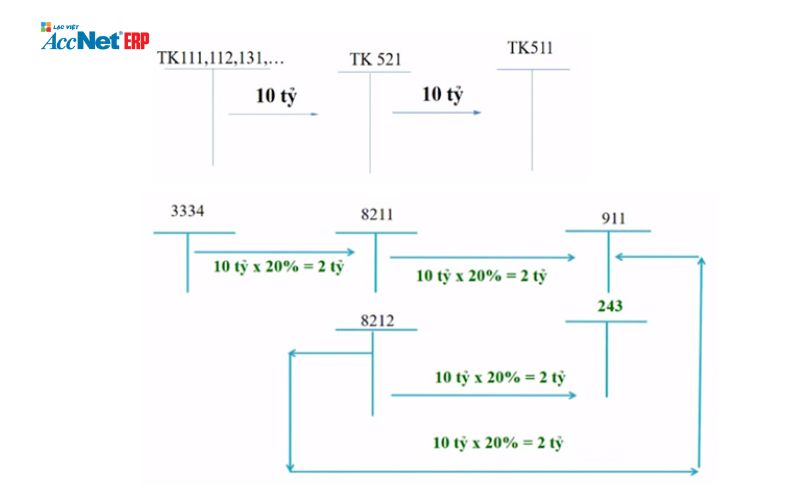

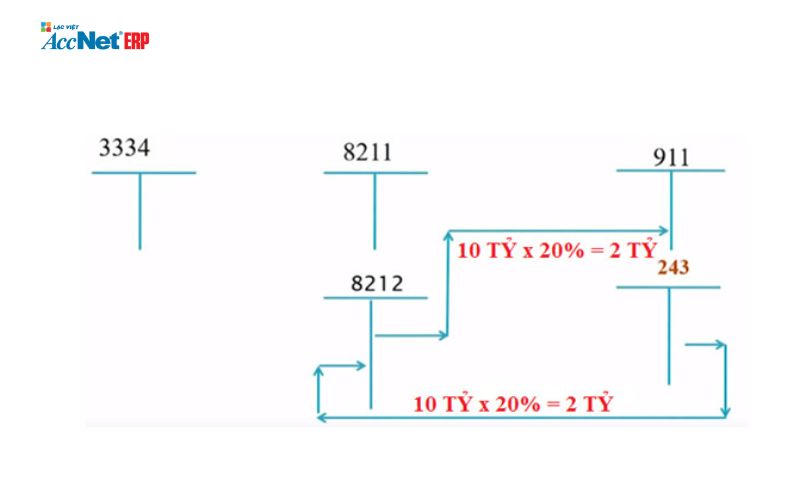

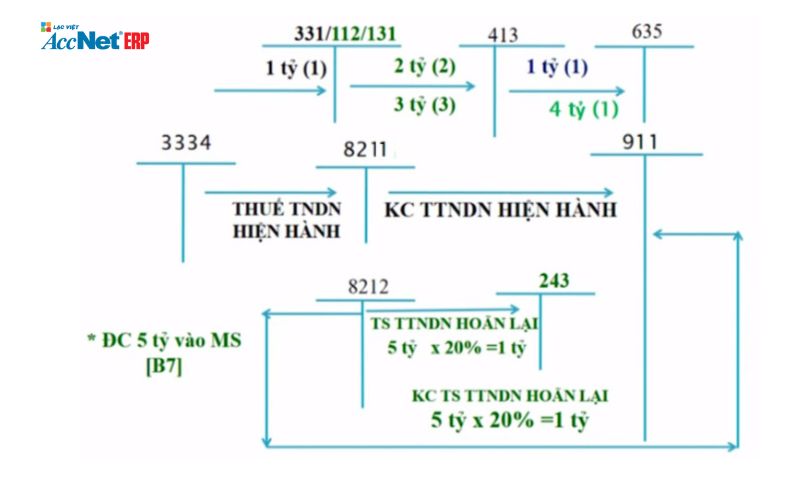

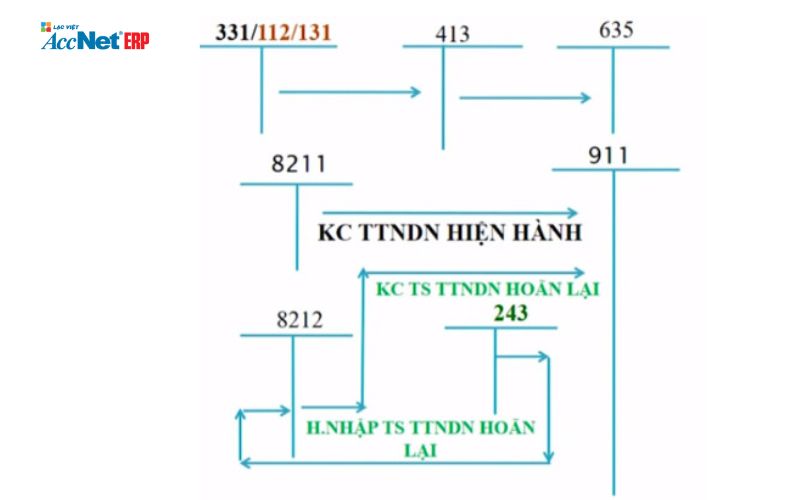

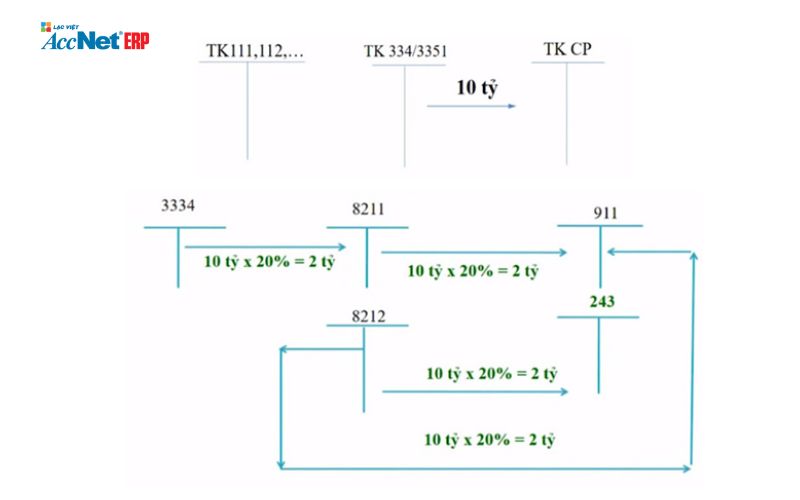

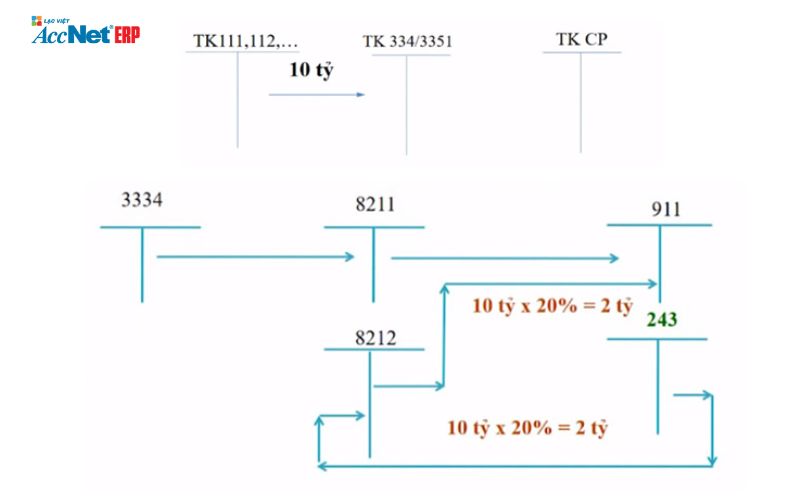

At year implementation report:Re-adjust the accounting and ledger, as follows:Diagram accounted for and adjusted ledgerMake adjustments on the declaration settlement reports CIT: tune into code [B2] 100 billion Codes, [B10] 80 billion.At year adjustment (the year in which they arise revenue):Re-adjust the accounting and ledger, as follows:Diagram accounting and adjust the accounting year adjustmentAdjust on the declaration settlement reports CIT: tune into settlement CIT code [B9] 100 billion; code [B3] 80 billion.

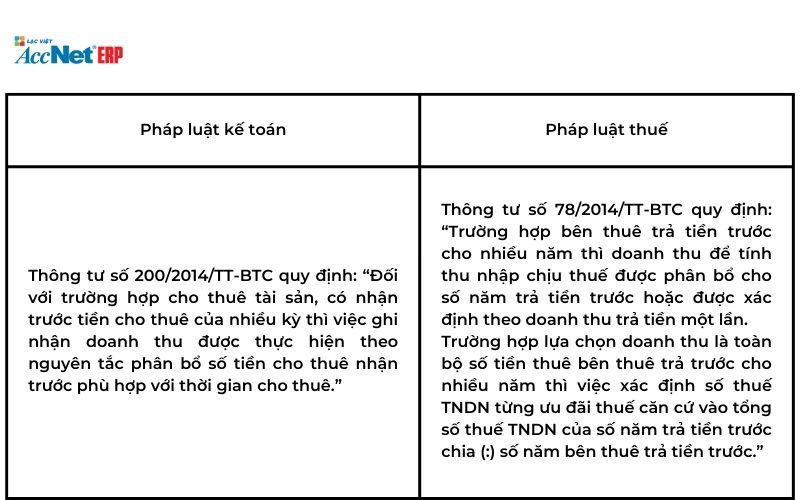

The guidelines for the recognition of revenue for rental property can vary between tax law and accounting regulations.

Example 2:

Date 01/01/2021 business ABC has leased a property in 02 years to receive money 01 is (13,2 billion/year (including VAT 10%) x 2 years = 26,4 billion). Business choose the method of calculating corporate INCOME tax 01. Suppose the current business ABC is 30% CIT reduction in 2021 the price of the capital of 2021 respectively of operational leasing of this property is 10 billion, other expenses is 0 clock. To revenue recognition, the leased property for the tax and accounting, to consider the following situations:Tax and accounting how to calculate corporate INCOME tax are different:

Corporate INCOME tax calculated on the total revenue for rental property during the year, even accounting can choose the method of calculating the revenue for each period of the lease individually.

In example 2, business ABC has chosen the method of calculating corporate INCOME tax 01 times, it would have recorded the entire rental income property (26,4 billion) in the year's first hire, 2021. If, however, use the method of calculating corporate INCOME tax in total revenue, then the business will have to split all revenue 26,4 billion for 2 years lease, each year is 13.2 billion, and subject to CIT in this total.

Tax and accounting have the time of revenue recognition, the different:

Accounting is often recorded sales for rental property according to the method of calculating rental property according to each period of the lease individually. Revenue will be recognized at the time of the end of the lease.

Meanwhile, CIT revenue recognition, the leased property in the year in which this revenue is incurred, regardless of the time of year.

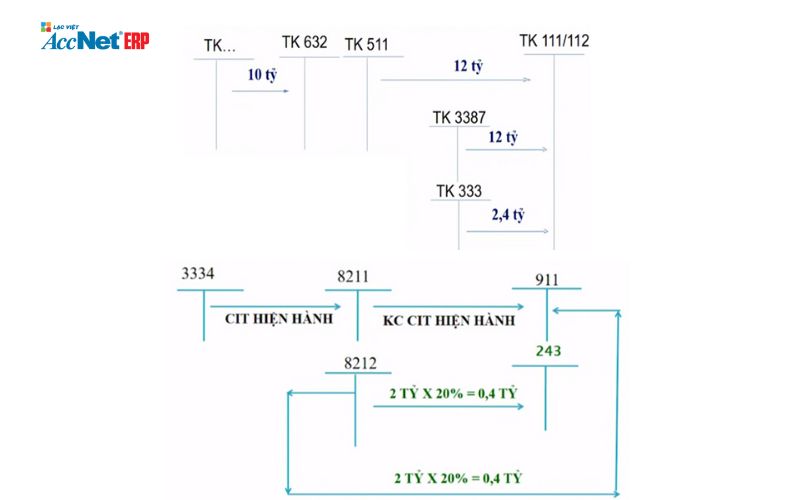

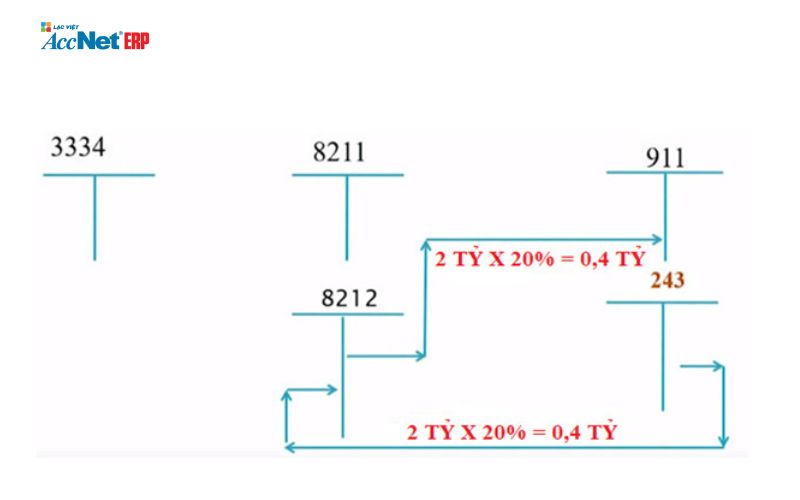

So, for example 2, the accounting of the business ABC will recognize revenue for the rental property at the end of year 2022, when the rental property this end. Meanwhile, CIT will burn the whole of the revenue in the year 2021, when the revenue is incurred. With 30% reduction of corporate INCOME tax year 2021, business ABC will be reduced by 30% on the tax payable in the year 2021, and there will be no reduction of corporate INCOME tax in the year 2022 when recorded sales for rental property.Guide to adjust the gap, for example 2 is as follows:At year implementation report:Re-adjust the accounting and ledger, as follows:The diagram illustrates the accounting and bookkeeping reporting yearMake adjustments on the declaration settlement tax the following year, the numbers in the code [B2] be adjusted up into 12 billion and in code [B10] is adjustable down to 10 billion. It is noteworthy that in this example, taxable income has increased due to business select the method of calculation of corporate INCOME tax 01 times, this means that business will not be entitled to preferential reduction of 30% corporate INCOME tax.At year adjustment (the year in which they arise revenue):Re-adjust the accounting and ledger, as follows:Diagram accounting and bookkeeping year adjustmentAdjustment instructions on the declaration settlement tax year 2022 of business:Year adjustment is the year 2022, the business need to adjust the two codes on the declaration settlement reports business income tax. First, tune into the code number [B9] in the amount of 12 billion. Then, tune into code [B3] in the amount of 10 billion.In addition, it should be noted that in the year 2022 business does not have preferential reduction of 30% corporate INCOME tax. This means the taxable income of the business will increase since there were no tax relief from the government. Therefore, enterprises need to calculate carefully and adjust the full information on the declaration, settlement tax per year to ensure compliance with the tax rules and avoid the risks incurred.

How to handle different about recorded trade discounts and promotion between the department of taxation and accounting

Account record account trade discounts under circular no. 200/2014/TT-BTC account is 521, according to circular no. 133/2016/TT-BTC account is 511.

About vat (VAT), then the sell-side will be adjusted up output VAT at the time of invoicing.

When businesses have the program discount in sales, invoicing recorded account trade discounts is very important to ensure accuracy in the recognition of expenses and income of the business. However, if the business has not billed recorded in discount, rebate and trade in the financial year, the recorded account trade discount on any invoice adjustment is necessary.

Example 3:

To illustrate this case, assuming Business XYZ has developed a program to trade discount in sales in fiscal year 2021. However, to date 31/12/2021, business has not yet billed recorded account, discount for customers. When to year 2022, new business invoicing adjustments to the recorded account trade discounts, the business must be recorded on the invoice adjustment. Business't be extracted before to the cost account trade discounts when not billed adjust this.

This case is very important for the calculation and determine the amount of VAT and income of the business. So, businesses need to pay attention and note to the invoice recorded account trade discounts right time to avoid errors in business process.

Example 4:

By 2021, the business DOCTOR can program trade discount to the customer (if the customer purchases reaching a turnover of 100 billion will be discounted 10%). But to date 06/01/2022 business DOCTOR new invoice discounting trade of goods sold to A customer achieve sales in year 2021 is 10 billion (100 billion x 10%), VAT is 1 billion and the bill was set before the time of submission of FINANCIAL report in 2021.

Example number 4, business, DOCTOR, has developed a program to trade discount for our customers in 2021. However, business was billed recorded account trade discount after payment of the financial statements for the year 2021.

The bill trade discount after submission of financial statements that can cause the problems related to accounting and VAT of the business. In this case, the business DOCTOR, had been shortcomings in the recorded account discount trade in financial year 2021. When business invoicing adjustments on 06/01/2022, businesses must calculate and submit VAT amount has been adjusted.

With these situations, businesses need to be cautious and pay attention to the recognition discounts right time to avoid errors in business process. This will help the business avoid the financial risk and ensure the accuracy in the recognition of expenses and income of the business.

Guide to adjust the gapAt year implementation report:Re-adjust the accounting and ledger, as follows:Suppose business does not have preferential tax year 2021, we have the diagram accounted for as follows:The diagram illustrates the accounting and bookkeeping reporting yearAdjust on the declaration settlement tax by year: tune into code [B2] is 10 billion.At year adjustment (the year in which they arise revenue):Re-adjust the accounting and ledger, as follows:Diagram accounting and bookkeeping year adjustment

2. Manual handling temporary differences related to cost on settlement tax by year

2.1 Related to cost

The account temporary differences related to cost is the expense that the difference between accounting law and tax law leads to the difference between accounting data and tax figures. The handling of temporary differences related to costs is done on the code number [B4], [B7], [B12]. The cost of this often causes the arising difference due to VAT, corporate INCOME tax and personal income tax. For example, the expenses depreciation of fixed assets, payroll costs, staff costs, the cost of marketing and advertising. To handle temporary differences related to costs, businesses need to make adjustments to accounting data and the corresponding entry on the settlement reports business income tax.

2.2 handling instructions on CIT returns in years when there is a difference between the way recorded the expenses on tax and accounting.

In accordance with Article 4 of circular no. 96/2015/TT-BTC on 22/6/2015 and Article 7 of circular no. 78/2014/TT-BTC on 18/6/2014 of the Ministry of Finance on corporate INCOME tax, expenses and income related to the evaluation of the item monetary assets and liabilities denominated in foreign currency is determined as follows:

The losses exchange rate differences exchange rate arises due to re-evaluate the item monetary assets and liabilities denominated in foreign currencies at the end of the tax period are not deducted when calculating taxable income CIT.

Only the losses exchange rate differences exchange due to the revaluation of debt to pay end of the period, the new tax is deducted when calculating the taxable income subject to corporate INCOME.

Account interest rate differentials, exchange rates arises due to re-evaluate the item monetary assets and liabilities denominated in foreign currencies at the end of the tax period, including variances exchange rates due to the revaluation of the balance by year-end, cash, deposits, money transfer and the account receivables of foreign currencies not included in income subject to corporate INCOME tax.

Example 5:

At the end of 2021, company ABC has re-evaluate the item monetary assets and liabilities denominated in foreign currency and incurred interest 1 billion on account of 331, and incurred losses 2 billion on account of 112 and 3 billion on account 131. Total losses arising is 5 billion to the debtor account, 413, while the total interest accrued is 1 billion side have an account, 413. Therefore, the difference between the pnl is 4 billion. To adjust this gap, ABC company need to subtract the cost of losses exchange rate differences exchange 4 billion in the financial statements of the year 2021.Guide to adjust the gap as follows:At year implementation report:Re-adjust the accounting and ledger, as follows:Diagram accounting and bookkeeping reporting yearAdjust on the declaration settlement tax by year:Assessment year: tune into code [B7] is a 5 billion. (Note: Code [B7] – The account adjustment increases the profit before tax other)At year adjustment (the year in which they arise revenue):Re-adjust the accounting and ledger, as follows:The diagram illustrates the accounting and bookkeeping year adjustmentSuppose in year adjustment, all the balances of the accounts, 112 and 131 has been spent in or out entire amount and is accounted for at the rate of bookkeeping. To adjust for difference, exchange rate, it should be implemented into the code of [B12] in the financial statements. Code [B12] is the difference between the rates bookkeeping and rates early recognition of accounts 112 and 131 in the following accounting period. This adjustment will reduce the profit before tax of another business.

2.3 guide how to solve the difference between tax and accounting related to the cost of wages

Under the provisions of circular no. 96/2015/TT-BTC, the expenses wages, salaries and allowances payable to workers expiration of the filing yearly tax practice has cost not deducted when determining taxable income. In addition, the expense accruals under any term, cyclical, which to the end of term, end of cycle, not yet spent or costs, not all also not be subtracted when determining taxable income.

Example 6:

according to the regulations of The office of 512/CT-WITHOUT, funds 13th month salary in 2021 and the year awards based on the business results and energy efficiency work 2020 year of the employee actually spent on 12 April 2021, and April 4, 2021, respectively, and is calculated into the cost is deducted when determining income subject to corporate INCOME tax year 2021. However, to be deductible, the expenses must meet the conditions specified and are guaranteed accurate, valid and valid documents as regulated by law.

Example 7:

Business case accruals bonus of 2021, but until the filing and settlement tax year 2021 remain unrealized cost, then the accruals will not be included in deductible expenses of 2021. If, however, to January 12, 2022 business make money, bonus accruals on the full bill and vouchers according to the rule of law, then the account details will be included in deductible expenses of the tax year 2022 (According to dispatch no. 1703/CT-WITHOUT date 05/03/2018 of City tax Department. Ho Chi Minh City).

Example 8:

At day 31/12/2021 company, CBA has incurred costs to pay salary and bonus in year 2021 is 10 billion, but to date 31/3/2022 company still has not spending this money that comes months 10/2022 business can afford to pay for this account.In accordance with Article 4 of circular no. 96/2015/TT-BTC, the fee accruals under any term, cyclical, which to the end of term, end of cycle, not yet spent or costs, not all the expenditures that are not deducted when determining taxable income. So, expenses salaries and bonus above has not been spent in 2021 will not be included in deductible expenses of 2021. Instead, when The company CBA is full of bills and vouchers to prove the expenditure for this account at the time after settlement tax year 2021, then the account details will be included in deductible expenses of the tax period, respectively.Guide to adjust the gap as follows:At year implementation report:Re-adjust the accounting and ledger, as follows:

Modified on declaration settlement tax: updates the amount of 10 billion into the code number [B4] for the expenditures are not deducted when determining taxable income.At year adjustment (the year in which they arise revenue):Re-adjust the accounting and ledger, as follows:

The information, knowledge about the report settlement tax CIT (báo cáo quyết toán thuế thu nhập doanh nghiệp) đã được phần mềm kế toán Accnet fully updated and most detailed. Hope the article helps businesses, accountants perform a full, accurate and correct term for any settlement.

Mai Huong

Have censored content

The editor for the accounting of Vietnam with over 5 years of experience. Stand out with the ability to analyze profoundly the accounting regulations, tax policies, standards financial statements. Read more >>>

Theme: