Over time, the fixed assets can at levels need improvement to continue to promote effective use. This is the time when the operation overhaul of fixed assets become key factors, requires the business to organize the implementation. In this article AccNet will provide detailed information, from basic concepts to the legal regulation, method of accounting major repairs of fixed assets-specific help businesses implement the right process, meet the requirements of modern accounting.

1. Accounting major repairs of fixed assets is what?

Accounting major repairs of fixed assets is the process of recognition of costs arising from the repair or renovation or upgrade fixed assets on bookkeeping business. The aim is to ensure that all costs are properly reflect the nature, in accordance with the provisions of law, the accounting standards.

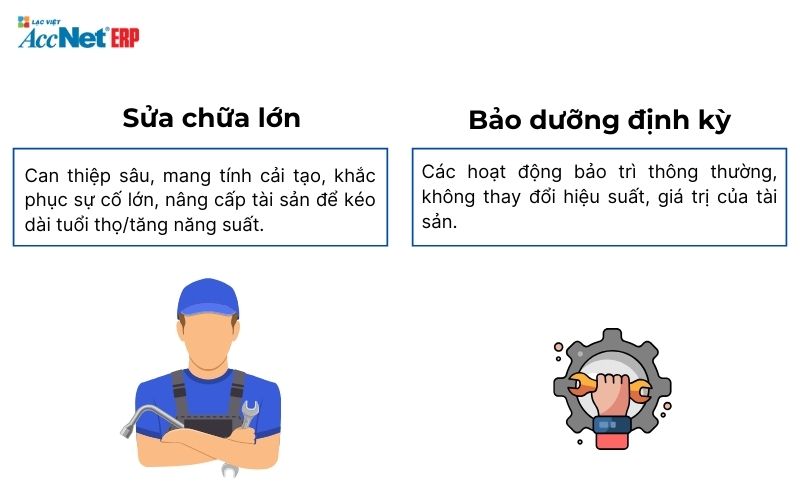

Difference between major repairs and periodic maintenance:

- Major repairs: intervene, bring improvement, troubleshooting, big upgrade properties to extend/increase productivity.

- Periodic maintenance: maintenance activities, usually, do not change the performance, the value of the property.

2. The method of accounting major repairs of fixed assets

2.1. Accounted for at cost in the states

Business accounting major repair costs directly to cost in the states when:

- Repair operations do not bring economic benefits long-term.

- Cost is not large enough to allocate or recorded increase of fixed assets.

- Processes and accounting entries accounting in particular:

Use accounts:

- TK 627: the Cost of joint production (apply with asset production service).

- TK 641: Cost of sales (applies to assets in active service sales).

- TK 642: Cost management business (applies to property that serves general manager).

Illustrative examples: Business repair air conditioning systems in office with cost of 20 million.

- Debt TK 642: 20.000.000

- Have TK 111/112: 20.000.000

Read more:

- Ghi sổ hao mòn TSCĐ giúp theo dõi tài sản chính xác nhất

- Accounting reduce fixed assets do thanh lý theo quy trình xử lý tài sản doanh nghiệp

- Hạch toán cho thuê tài sản cố định theo hợp đồng thuê ngắn/dài hạn

2.2. Accounting major repairs of fixed assets when allocating gradually over the states

Repair costs are allocated gradually over the accounting period when:

- Repair costs are of great value.

- Costs incurred do not change the original asset prices but bring economic benefits in many states accounting.

Accounting accounting major repairs of fixed assets, in particular:

- TK 242: prepaid Expenses long-term.

- TK 627, TK 641, or TK 642: Recorded cost allocated to each period.

Illustrative examples: Business overhaul production lines, with a cost of 500 million allocated in 5 states accounting.

- Debt TK 242: 500.000.000

- Have TK 111/112: 500.000.000

Allocated to each accounting period:

- Debt TK 627: 100.000.000

- Have TK 242: 100.000.000

2.3. Accounting major repairs of fixed assets when recording increase the original price fixed assets

Repair costs are recorded increase of fixed assets when:

- Repair operations significantly improve the performance, longevity, use value of fixed assets.

- Repair cost pass a certain value, that meets the criteria noted in fixed assets.

Accounting entries accounting in particular:

- TK 211: Record the original price fixed assets.

- TK 214: Recorded amortization, respectively (if available).

Illustrative examples: Business upgrade systems, machinery with a cost of 800 million, extend the life more 5 years.

- Debt TK 211: 800.000.000

- Have TK 111/112: 800.000.000

3. The accounting entries accounting major repairs of fixed assets

3.1. Overhaul does not change original price

Situations apply: Business only fix damaged or performing maintenance activities in depth, which does not improve the value of the property.

Illustrative examples: repairing large power system office at a cost of 50 million.

- Debt TK 642: 50.000.000

- Have TK 111/112: 50.000.000

3.2. Accounting major repairs of fixed assets when major repairs alter original price

Situations apply: Business renovated properties to increase productivity or value in use, for example: system upgrade production line.

Illustrative examples: upgrading industrial printer at a cost of 300 million.

- Debt TK 211: 300.000.000

- Have TK 111/112: 300.000.000

3.3. Cost allocation overhaul across the states

Situations apply: the Cost of major repairs of great value, should be allocated gradually over many states to not greatly affect the profitability of a single.

Illustrative examples accounting major repairs of fixed assets for the above case: repair large production line, with a cost of $ 600 million, allocated in 3 states accounting.

- Debt TK 242: 600.000.000

- Have TK 111/112: 600.000.000

The amounts allocated to each period:

- Debt TK 627: 200.000.000

- Have TK 242: 200.000.000

4. The legal regulations related to accounting major repairs of fixed assets

4.1. The text current legislation

Accounting major repairs of fixed assets to comply with the provisions from the text of the legislation below:

- Circular no. 200/2014/TT-BTC

- Circular 45/2013/TT-BTC

- The accounting law of 88/2015/QH13

4.2. Accounting principles overhaul of fixed assets

The important principles when performing accounting include:

Guaranteed repair cost is allocated in the correct accounting period, avoiding the recorded deviations affect the financial statements.

Condition record increase of fixed assets:

- The repair operation to bring economic benefits in the future.

- The cost to renovate pass the value of an accounting period, there is significant impact on the value of fixed assets.

5. Important note when accounting major repairs of fixed assets

5.1. Clearly define the purpose, type of repair

Businesses need to clearly distinguish the type of repair to the accounting match:

- Overhaul brings renovated: recorded at the original price fixed assets.

- Major repairs to fix the damage: can be recorded at cost in the states or allocated by the states.

- Periodic maintenance: do Not under accounting major repairs, which were recorded directly into cost management/production.

5.2. Check/store vouchers in full when accounting major repairs of fixed assets

To ensure the legitimacy of the accounting, business need to store complete the following documents:

- Inspection records of fixed assets: Assessment of the status and reason for repair.

- Contract repair: Attached under the terms of cost, time taken.

- Minutes acceptance fix: recognition results, corrected values was made.

- Bills, proof of payment: invoices from contractors or unit to make repairs.

5.3. Ensure compliance with legal regulations

Accounting major repairs of fixed assets should comply with the regulations of the Ministry of Finance to avoid the error like:

- Remember mistaken into the cost in the states instead of recording increase of fixed assets.

- Recorded a one-time cost rather than allocated by the states.

- Businesses need to regularly update the text of laws, accounting standards to ensure the accounting fit.

6. Modern solution for management and accounting major repairs of fixed assets

Management software fixed asset modern business help optimize the management, accounting major repairs, with benefits such as:

- The software automatically classifies the cost of major repairs, accurately recorded into account accordingly.

- Supports the calculation, allocation, repair costs through the accounting period.

- Status update repair, residual value of assets in real-time.

Một số phần mềm tiêu biểu tại Việt Nam như Phần mềm AccNet Asset cung cấp giải pháp toàn diện, thân thiện với người dùng.

SOFTWARE ACCNET ASSET – STOP WASTING ASSETS

- Cut reduction by 15-20% repair costs each year thanks to proper maintenance term

- 50% discount time inventory, and reporting of property

- Avoid losses hundreds of millions of since the property is "missing the mark", using the wrong purpose

- Increase asset life cycle up minimum 25% thanks to the tracking and timely warning

- Reduce errors depreciation – is not tax arrears

A business average savings from 300 to 500 million/year after deployment AccNet Asset

SIGN UP CONSULTATION AND DEMO TODAY

Hạch toán sửa chữa lớn tài sản cố định không là một hoạt động kỹ thuật đòi hỏi sự chính xác trong quản lý. Việc áp dụng đúng phương pháp hạch toán sẽ giúp doanh nghiệp minh bạch tài chính. Các giải pháp phần mềm công nghệ hiện đại là trợ thủ đắc lực, hỗ trợ doanh nghiệp quản lý tài sản hiệu quả hơn. Hãy bắt đầu ngay hôm nay bằng cách tìm hiểu, triển khai các công cụ quản lý tài sản cố định tiên tiến AccNet Asset. Đừng để tài sản cố định trở thành gánh nặng, hãy biến chúng thành lợi thế bền vững cho doanh nghiệp của bạn!

CONTACT INFORMATION:- ACCOUNTING SOLUTIONS COMPREHENSIVE ACCNET

- 🏢 Head office: 23 Nguyen Thi huynh, Ward 8, Phu Nhuan District, ho chi minh CITY.CITY

- ☎️ Hotline: 0901 555 063

- 📧 Email: accnet@lacviet.com.vn

- 🌐 Website: https://accnet.vn/

Theme: