Compliance with regulations property tax is a legal obligation, the key element in the management of business finance. One of the key taxes that businesses need main interest is tax for rental property. However, many businesses still have difficulty in determining the right level of tax calculation procedures for filing. Understand that, this article AccNet will provide detailed instructions, from basic concepts to the legal provisions, the way made for business.

1. Excise for hire what is a property?

Tax for rental property applies to businesses or individuals that have business activities property for rent, including:

- Real estate: Houses, offices, factories.

- Equipment, means of transport, automobile, industrial machinery.

- Other assets: Asset production service or business.

Points peculiarities of the excise in the field of rental property:

- Apply to revenue arising from the operation for rental property.

- The specific depending on the type and scale of business.

2. Legal provisions related to tax rental property

2.1. Legal grounds

Excise specified in the text of the legislation below:

- Decree 126/2020/ND-CP: detailed instructions about tax obligations for business activities, including property rental.

- Thông tư 302/2016/TT-BTC: Quy định mức thu thuế môn bài, các trường hợp được miễn giảm.

- The law on tax Administration no. 38/2019/QH14: The legal basis of the obligation to declare and pay tax.

2.2. Subject to excise tax for rental property

An excise tax applies to:

- Business: including private enterprises, joint stock companies, LIMITED company or cooperative.

- Business individuals: The individual or business group activities for rental property.

- Economic organization other: As branches and representative offices involved in business property rental.

The case for reducing tax:

- New business establishment is free of tax in the first year.

- Business has a turnover below the level specified.

- The organization operate for the public benefit or not arising revenue from property rental.

2.3. The level of tax for rental property

Excise tax is determined based on:

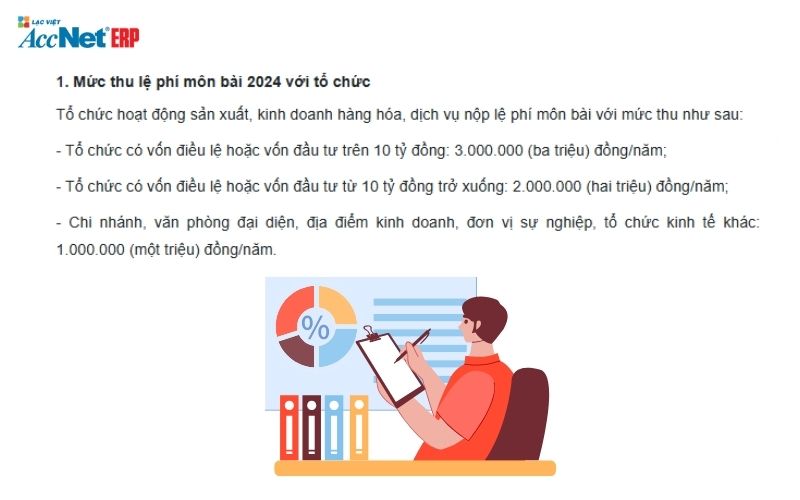

Charter capital: With the business, the level of income based on capital business registration.

- The charter capital of 10 billion: 3 million/year.

- Charter capital from 10 billion back down: 2 million/year.

Annual revenue: With business, the revenue is calculated as revenue from operations for rental property.

- Revenue 500 million/year: 1 million/year.

- Revenue from 300 - 500 million/year: 500,000/year.

- Revenue less than 300 million/year: tax-Free license.

3. How to calculate tax for rental property

Tax is calculated based on two main factors:

- For business: The tax base in the charter capital or capital investment recorded on the certificate of business registration.

- For individual business: tax Rates based on annual revenue from leasing the property.

Formula for calculating the tax for rental property:

- Business: Tax = tax Rate fixed by the charter capital.

Example for business: Business with A charter capital of vnd 15 billion, active in the field for real estate rental.

Excise rates: 3,000,000 vnd/year (applicable for business charter capital of 10 billion).

- Of private business: Tax = annual turnover × the Rate specified (if the revenue is below the tax-free will not apply).

For example, for individual business: business B for rent with annual sales of 450 million.

Excise rates: 500,000/year (applies to revenue from 300 - 500 million).

Read more:

- Thực hiện nghĩa vụ nộp thuế môn bài đầy đủ ngay từ đầu năm tài chính

- Accounting tax chi tiết theo Thông tư 200 chuẩn kế toán

4. Procedure declaration and submission of tax for rental property

4.1. Record declaration tax

Business/personal need to prepare the following records to declare tax:

Business:

- Declaration excise (according to form no. 01/fee license issued together with circular 302/2016/TT-BTC).

- Business registration certificate.

- Contract for rental property.

Business:

- Contract for rental property.

- Prove identity or identification citizens.

4.2. The deadline to declare and pay tax for rental property

New business established:

- Declare tax within 30 days from the date of issuance of the business license.

- License tax before the date 30/01 every year.

Business: tax declaration when the revenue is earned from leasing the property.

4.3. Method of filing tax

Business and business can choose the method of filing tax for rental property follows:

Submitted directly to the tax authorities: through the trading room/department tax revenues of local time.

Submitted through the electronic system:

- Đăng nhập vào Cổng thông tin thuế điện tử (https://thuedientu.gdt.gov.vn).

- Create and send declarations excise tax online.

- Make tax payment via bank transfer.

5. The important note when doing taxes for rental property

5.1. Identify the right audience and excise rates for rental property

Identifying the right subject to tax and the tax rate is the determining factor to ensure compliance with legal regulations. The note includes:

- Distinguish between taxable and tax-free: The new business establishment or business have revenue below the specified threshold to be tax-free license.

- Ensure proper recognition rate tax: Based on regulatory capital (for business) or revenue (for individual business).

5.2. Check and store vouchers full

Businesses need to prepare/store the following documents to ensure the declare and pay tax for rental property precision:

- Contract for rental property with full information about the property, rental value, contract term.

- Business registration certificate/permit to operate.

- Stock from payment of excise for reference when necessary.

5.3. Handle the case of violation

Business may face penalties if violations of the excise, including:

- Declaration slow or improper term: penalty as a percentage on the amount of tax payable.

- Filing late tax: charged interest for late payment daily.

For example: If the business does not pay tax due, the penalty can be up to 20% of tax payable, plus interest for late payment under current regulations.

6. Solution optimization implementing tax for rental property

Việc áp dụng phần mềm AccNet Asset giúp doanh nghiệp/hộ kinh doanh giảm thiểu sai sót, tiết kiệm thời gian trong việc kê khai/nộp thuế môn bài cho thuê tài sản. Một số lợi ích bao gồm:

- Tự động tính toán thuế: Phần mềm AccNet Asset hỗ trợ xác định chính xác mức thuế môn bài dựa trên thông tin doanh thu/vốn điều lệ.

- Tax declaration online: built-in feature to submit a tax return online through the electronic system.

- Storage/voucher management: store entire records and documents related easy lookup when needed.

Phần mềm AccNet Asset là lựa chọn lý tưởng, mang lại giải pháp toàn diện cho doanh nghiệp trong việc quản lý kế toán - thuế.

SOFTWARE ACCNET ASSET – STOP WASTING ASSETS

- Cut reduction by 15-20% repair costs each year thanks to proper maintenance term

- 50% discount time inventory, and reporting of property

- Avoid losses hundreds of millions of since the property is "missing the mark", using the wrong purpose

- Increase asset life cycle up minimum 25% thanks to the tracking and timely warning

- Reduce errors depreciation – is not tax arrears

A business average savings from 300 to 500 million/year after deployment AccNet Asset

SIGN UP CONSULTATION AND DEMO TODAY

Thuế môn bài cho thuê tài sản không chỉ là nghĩa vụ pháp lý mà còn là yếu tố quan trọng trong việc duy trì hoạt động kinh doanh. Doanh nghiệp nên cân nhắc áp dụng các giải pháp số hóa, phần mềm kế toán hiện đại. Phần mềm AccNet Asset là một trong những công cụ hỗ trợ đắc lực, mang đến sự tiện lợi, chính xác trong quản lý thuế môn bài cũng như các nghiệp vụ kế toán khác.

CONTACT INFORMATION:- ACCOUNTING SOLUTIONS COMPREHENSIVE ACCNET

- 🏢 Head office: 23 Nguyen Thi huynh, Ward 8, Phu Nhuan District, ho chi minh CITY.CITY

- ☎️ Hotline: 0901 555 063

- 📧 Email: accnet@lacviet.com.vn

- 🌐 Website: https://accnet.vn/

Theme: