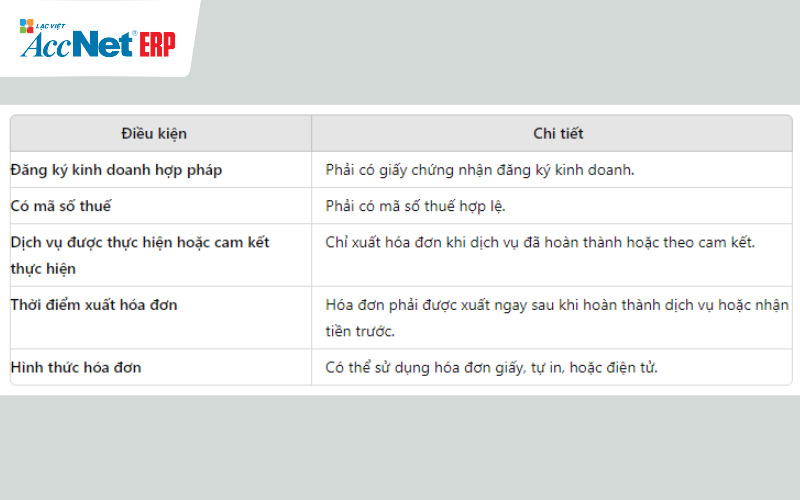

1. Regulations on conditions invoice shipping

- Business of providing transportation services must be a registered legal business

- Business must have a tax code, registered tax declaration to the tax authority.

- The shipping bill is only when shipping service has been made under the contract/agreement between the parties involved.

- Invoice must be produced immediately after the service completion/receipt payment in advance (if any) under Article 9 of Decree 123/2020/ND-CP, Article 4 circular 78/2021/TT-BTC.

- Businesses can use paper bills, invoices or electronic invoices according to the needs, abilities, according to the Decree 123/2020/ND-CP.

2. Content regulations/time invoiced shipping

2.1. Mandatory content on the bill

- Name, address, tax code of the unit that provides shipping services.

- Name, address, tax identification number (if any) of the service recipient.

- Description shipping service, type of goods, means of transport, points go/destination, distance shipping.

- Unit price, quantity, total value of service tax, the amount of VAT.

- Date invoicing and signature of the invoice.

2.2. The time of invoice

Invoice must be produced at the completion of the services or upon receipt of money payment in advance, specified in detail in specified on the invoice shipping Article 9 of the Decree 123/2020/ND-CP.

Read more:

- Regulation bill latest electronic theo Thông tư 78 và Nghị định 123

- Quy định về hóa đơn của hộ kinh doanh theo Nghị định 123 mới nhất

- Dispatch processing bill illegal theo quy định của Bộ Tài chính

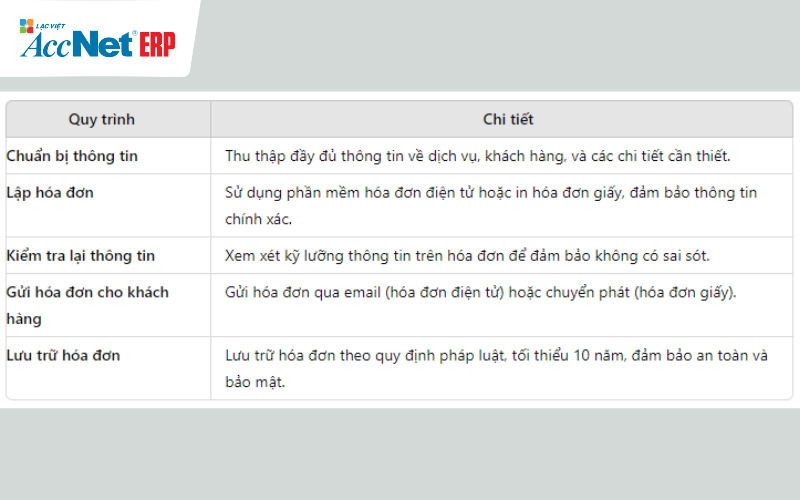

3. Regulations on the export process, the shipping bill

- Fully collect the necessary information from the client, details about the shipping service.

- Use software electronic invoice/bill printing paper. Ensure the invoice include all the information required under Article 4 of Decree 51/2010/ND-CP.

- Invoices can be sent via email (for electronic invoice) or delivered directly (for paper bills).

- Ensure the storage of invoices under the provisions of the accounting Law and the related regulations.

4. Regulations regulator/destroyed/lost bills

4.1. Adjust the bill

Article 19 of Decree 123/2020/ND-CP specified on the invoice shipping adjust set:

- Invoice false customer name, tax code, quantity of goods, value of services, businesses need to invoice adjustment.

- Change value service after the invoice, the adjustment needs to be done to accurately reflect the transaction.

4.2. Cancel invoice

According to the Decree 123/2020/ND-CP, Article 20 stipulates cancel invoice:

- Transportation services has the invoice, but not done (for example, cancel your orders/customers do not use the service), businesses need to cancel the invoice has.

- Case errors are detected before sending the invoice to the customer, the business can get receipts and invoicing new without billing adjustments.

4.3. Loss or damage bill

Based on the Decree 51/2010/ND-CP, Article 22 and the Decree 123/2020/ND-CP, Article 21 (supplement), specified on the invoice shipping when handling the case of loss or damage is as follows:

- Lost receipts/fire/broken before establishment, businesses need to immediately notify the tax authorities. Specify the number of bills lose or damage any measures were taken to overcome.

- Business establishment memorandum of the issue, then notify the tax agency establishment bill new replacement in case of invoices issued but not yet sent to the customer

- If the invoice was drawn up and sent to customer but then lost, burnt, damaged, both sell-side/buy-side set up a memorandum of the work. Businesses can set up alternative bill or invoice copy, depending on the specific situation.

Read more:

- Circular 78 of electronic invoices bắt buộc áp dụng trên toàn quốc

- Latest regulations on export invoices theo Thông tư 78 và 219

- Hướng dẫn chi tiết về quy định hóa đơn bán lẻ current

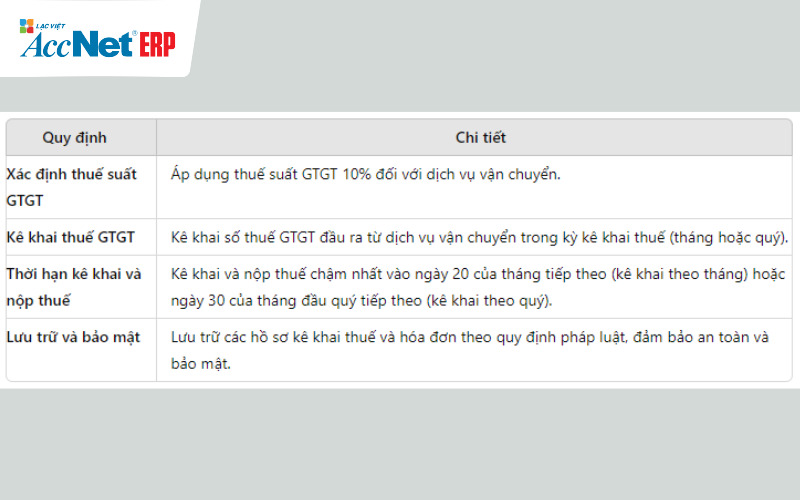

5. Specified tax declaration from the bill shipping

The tax declaration from the bill shipping must comply with the provisions of the Law on value added Tax (VAT), includes:

- Shipping services usually apply VAT is 10%, as specified in Article 8, Law on VAT 13/2008/QH12, amended by Law no. 31/2013/QH13 and Law no. no. 71/2014/QH13.

- Business declare the full amount of VAT output from the shipping services during the tax declaration (month or quarter) as specified in The 10, circular 156/2013/TT-BTC date 06/11/2013 of the Ministry of Finance.

- VAT from the shipping service must be filed within the time limit specified on the invoice shipping, i.e. at the latest on the 20th day of the next month for business declaration according to months, and on January 30 of the first month of the next quarter for the business declaration under you.

6. Specified storage/security upon the shipping bill

6.1. Duration of storage: Bills (paper/electronic) must be stored a minimum of 10 years in Article 41, the Law on accounting of 88/2015/QH13.

6.2. Storage method:

- Paper invoices: storage in filing cabinet with lock, storage safety, avoid damage.

- Electronic invoice: storage on safety systems, backup periodically, according to Article 11 of Decree 123/2020/ND-CP.

6.3. Security:

- Paper invoices: stored in a locked cabinet, limit removed.

- Electronic invoice: security encryption with the security measures network, according to Article 17, the circular 78/2021/TT-BTC.

Learn more:

- Hướng dẫn chi tiết về quy định hóa đơn trực tiếp current

- Hướng dẫn chi tiết nội dung nghị định 123/2020/NĐ-CP latest

- Hướng dẫn chi tiết nội dung nghị định 119 về hóa đơn điện tử

Compliance specified on the invoice shipping là một bước đi chiến lược giúp doanh nghiệp tránh khỏi những rủi ro không đáng có, mở ra những cánh cửa mới cho sự hợp tác, tin tưởng từ khách hàng/đối tác. Hóa đơn vận chuyển là chứng từ tài chính cho sự cam kết của doanh nghiệp đối với chất lượng dịch vụ cung cấp. Khi nắm rõ quy định, doanh nghiệp sẽ không chỉ đảm bảo tuân thủ pháp luật mà còn tối ưu hóa quy trình tài chính. Để nâng cao hiệu quả tự động hóa quy trình này, lựa chọn buy software electronic invoice là một bước đi thông minh, giúp doanh nghiệp dễ dàng quản lý, xuất hóa đơn nhanh chóng hơn.

Việc xuất hóa đơn vận chuyển là một khâu quan trọng nhưng thường bị bỏ qua hoặc xử lý sai cách, dẫn đến những rủi ro pháp lý, tài chính không đáng có. Theo quy định hiện hành, doanh nghiệp cần đảm bảo hóa đơn vận chuyển được xuất đúng thời điểm, đầy đủ thông tin về giá cước, thuế suất, các chi tiết liên quan. Sai sót nhỏ như chậm xuất hóa đơn hay thiếu thông tin có thể dẫn đến phạt hành chính hoặc mất uy tín trong mắt đối tác.

Vậy làm thế nào để đảm bảo mọi hóa đơn vận chuyển luôn tuân thủ quy định mà không mất quá nhiều thời gian? Hãy để software release bill of sale AccNet eInvoice hỗ trợ bạn với tính năng tự động hóa, chuẩn xác, cập nhật liên tục theo pháp luật. Trải nghiệm ngay để tối ưu quy trình xuất hóa đơn của doanh nghiệp!

PHẦN MỀM HÓA ĐƠN ĐIỆN TỬ ACCNET EINVOICE

TÍCH HỢP XUẤT HÓA ĐƠN TỪ MÁY POS - SÀN TMĐT

AccNet eInvoice được thiết kế như một nền tảng quản lý hóa đơn điện tử toàn diện, tích hợp sâu vào hệ thống tài chính – kế toán – bán hàng của doanh nghiệp. Đây không chỉ là công cụ phát hành hóa đơn, mà còn là giải pháp giúp tối ưu toàn bộ quy trình vận hành liên quan đến hóa đơn điện tử. Với AccNet eInvoice, doanh nghiệp có thể:

- Tạo và phát hành hóa đơn chỉ trong chưa đầy 30 giây, đảm bảo tốc độ và tính chính xác cao.

- Ký số trực tiếp ngay trên phần mềm, loại bỏ nhu cầu chuyển đổi file qua các công cụ trung gian, tiết kiệm đáng kể thời gian và chi phí.

- Tự động hóa toàn bộ quy trình từ nhập liệu, gửi email cho khách hàng đến lưu trữ hóa đơn, giúp giảm thiểu thao tác thủ công và hạn chế tối đa rủi ro sai sót.

- Kết nối liền mạch với hệ thống kế toán, bán hàng và ngân hàng điện tử, tạo nên một dòng chảy dữ liệu xuyên suốt trong toàn bộ hoạt động tài chính.

- Đồng bộ dữ liệu theo thời gian thực, mang lại sự minh bạch, chính xác và hỗ trợ ban lãnh đạo đưa ra quyết định kịp thời.

TÍCH HỢP XUẤT HÓA ĐƠN TỪ MÁY POS - SÀN TMĐT (RA MẮT 2025)

Một trong những điểm khác biệt nổi bật của nền tảng này là khả năng tích hợp xuất hóa đơn ngay từ máy POS tại cửa hàng bán lẻ và từ các sàn TMĐT lớn như Shopee, Lazada, Tiki… Cụ thể, với AccNet eInvoice:

- Xuất hóa đơn trực tiếp từ máy POS: Khi khách hàng thanh toán tại điểm bán hàng, hóa đơn điện tử được sinh ra ngay lập tức trên thiết bị POS, giúp giảm thiểu tối đa thao tác thủ công cũng như thời gian trì hoãn — toàn bộ giao dịch đều được ghi nhận & xử lý nhanh chóng, chuẩn xác.

- Tích hợp với sàn thương mại điện tử: Doanh nghiệp có thể kết nối dữ liệu đơn hàng từ các sàn TMĐT phổ biến, đồng bộ thông tin bán hàng, rồi phát hành hóa đơn tự động từ hệ thống AccNet. Việc này giúp tránh sai sót, tiết kiệm thời gian so với xuất hóa đơn thủ công từ file excel hay nhập dữ liệu tay.

- Đồng bộ hóa – lưu trữ & quản lý một cách liền mạch: Các hóa đơn phát sinh từ POS hoặc các sàn TMĐT được tích hợp vào hệ thống kế toán – lưu trữ hóa đơn đầu ra đầy đủ, cho phép tra cứu nhanh chóng, hỗ trợ trình tự kê khai thuế, đối soát doanh thu theo từng kênh.

- Tối ưu quy trình, giảm sai sót: Với tự động nhập liệu, ký số trên phần mềm, gửi hóa đơn cho khách hàng qua email hoặc các kênh số, doanh nghiệp giảm thiểu hầu hết các bước thừa, tránh được lỗi nhập tay hoặc mất dữ liệu.

✅ Số hóa hóa đơn – Tối ưu quản trị doanh nghiệp

- Discount 80–90% chi phí in ấn, chuyển phát, lưu kho

- Rút ngắn 70% thời gian xử lý, tăng hiệu suất kế toán

- Hóa đơn phát hành – tiền về nhanh hơn, cải thiện dòng tiền

- Hạn chế tối đa sai sót nghiệp vụ, minh bạch hóa dữ liệu

- Nâng cao trải nghiệm khách hàng nhờ tra cứu & thanh toán tiện lợi

✅ Tích hợp toàn diện cùng AccNet ERP

- Tự động hạch toán doanh thu ngay khi phát hành hóa đơn

- Phiếu thu/chi lập tức khi có biến động ngân hàng

- Updated công nợ & số dư real-time

- Hóa đơn gắn kết chứng từ gốc & báo cáo tài chính – đối chiếu nhanh, báo cáo chuẩn

✅ Chi phí hợp lý – Lợi ích vượt trội

- Gói cơ bản chỉ từ vài trăm nghìn đồng

- Phù hợp cả doanh nghiệp nhỏ lẫn tập đoàn lớn

- Đầu tư một lần – tận dụng lâu dài, dễ dàng mở rộng theo nhu cầu

ĐĂNG KÝ NHẬN DEMO NGAY

Vui lòng điền các thông tin vào form chúng tôi sẽ liên hệ lại với bạn trong 24h làm việc.

KHÁCH HÀNG TIÊU BIỂU ĐÃ VÀ ĐANG TRIỂN KHAI ACCNET EINVOICE

✅ Demo miễn phí full tính năng

✅ Báo giá cá nhân hóa theo quy mô doanh nghiệp

✅ Tư vấn 1:1 cùng chuyên gia có nhiều kinh nghiệm

- ACCOUNTING SOLUTIONS COMPREHENSIVE ACCNET

- 🏢 Head office: 23 Nguyen Thi huynh, Ward 8, Phu Nhuan District, ho chi minh CITY.CITY

- ☎️ Hotline: 0901 555 063

- 📧 Email: accnet@lacviet.com.vn

- 🌐 Website: https://accnet.vn/

Theme: